by Brian J. McCormick, guest columnist

When I began writing this column in 2013, I focused on China as a source of better-priced chemicals. I took note then of a 2011 Deloitte forecast that China was on the verge of surpassing the US in total chemicals sales. Time to gauge the degree to which this shift has occurred and the impact on prices.

I am going to home in on the trade data for the basket of 10 chemicals, selected to represent the petrochemical, inorganic, metals, and biofuel sectors, that make up the Datamyne US Best Price Benchmark. (You can see the March 2015 Benchmark on the Datamyne home page.)

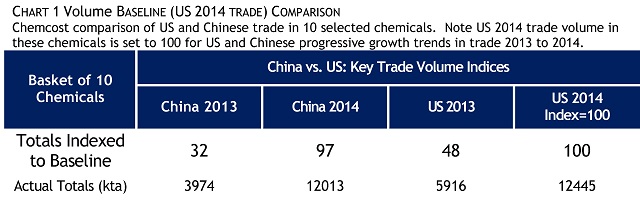

The baseline for comparison is 2014 US trade volumes which, for ease of reading variations, I’ve set to 100.

In Chart 1 below, China’s 2013 and 2014 trade volumes, and US 2013 trade volumes in the Benchmark chemicals are compared to the US 2014 baseline value.

This high-level view suggests a growth rate of 203% for China and 108% for the US, in this selection of chemical commodities, at least. The data confirms that both the Chinese and US chemicals markets are expanding, but China’s growth rate was faster in 2014. In just one year, the Chinese market – with a 97 Index – achieved approximately the same size as that of the US in 2014 (100 Index).

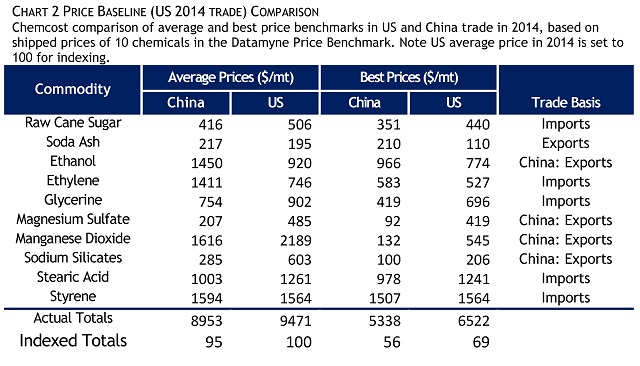

Next we explore best pricing opportunities for China and the US. To better dimension best price opportunities, Chemcost compared final 2014 price indices in Chart 2 below for the same basket of 10 commodities for the US and China based on both average and best benchmark prices. Again, we’ve set our baseline, US average prices in 2014, to 100 for ease of comparison.

Note that the best price benchmark was frequently but not always below the average US price. Based on these price benchmark and volume results for 2014, we observed other market factors:

- Trade basis in China appeared in better balance than in its recent past, with an even mix of imports and exports.

- Many best chemicals prices may be both outside and inside US and China.

- If you are shopping for inorganic chemicals or metals – with the exception of soda ash – China offered some favorable prices for cost savings (as we noted in the Chemcost blog in August 2013).

In general, we can conclude that a single-minded focus on average pricing will likely yield limited cost savings, e.g., roughly + 5%. In other words, you must diligently search for the best price to achieve it.

Best price focus in this comparison yields up to a 30% to 43% savings on an unconstrained opportunity basis for current chemical customers in both regions.

Note that this is “unconstrained” opportunity. Chemcost cautions that actual global material experience teaches a caveat must be clearly understood. A US chemical customer considering off-shore chemical sourcing must have the capability to do due diligence at the source – to ensure logistics, material quality and compliance aspects, and so sustain a final low price. One should always factor in the added costs of technically qualifying and sustaining off-shore chemical sources.

Take-away:

- For the Datamyne Benchmark basket of 10 commodities, the trade data lends support to the view that China will surpass the US in chemicals sales in 2015.

- Big cost savings opportunity can be found – up to 30% in the US – if customers utilize a volume-centric focus to research and identify best chemical prices. The opportunity rises as high as 43% if you include China and outside China supply sources.

- Local diligence and technical discipline will be required to ensure delivery and price excellence for off-shore chemical qualifications.

Finally, a comment: To many US customers in the past, China could be dismissed as being too far away and perhaps irrelevant to its supply strategy. Based on this limited basket of commodities, data suggests China leads the world in chemicals sales in 2015. Engaged chemicals market entrepreneurs must understand the world’s largest chemicals market – wherever that might be.

Chemcost Interactive LLC© 2014

About Brian J. McCormick

Brian J. McCormick was instrumental in developing procurement costing and quality assurance for P&G over a 34-year career. He is the founder and managing director of Chemcost Interactive LLC* (CI), a company providing research and analysis to support cost-efficient supply chain management.

Brian J. McCormick was instrumental in developing procurement costing and quality assurance for P&G over a 34-year career. He is the founder and managing director of Chemcost Interactive LLC* (CI), a company providing research and analysis to support cost-efficient supply chain management.

Chemcost can assist Datamyne’s customers in identifying lower price opportunities through consulting and training. Chemcost offers annual subscriptions to global and regional price bulletins on 225 commodities across 8 major chemical spend classes. Chemcost also offers recent dynamic should cost analysis (SCA) for many critical polymers, biochemicals and chemical commodities. Learn more and contact Chemcost at www.chemcostinteractive.com.

The opinions expressed in this article are those of its author and do not purport to reflect the opinions or views or Descartes Datamyne. In addition, this article is for general information purposes only and it’s not intended to provide legal advice or opinions of any kind and my not be used for professional or commercial purposes. No one should act, or refrain from acting, based solely on this article without first seeking appropriate legal or other professional advice.

* Chemcost Interactive is a trademark of Chemcost Interactive LLC