The race is on to secure essential resources, driving fierce global competition in critical mineral trade. Descartes Datamyne reveals how the competition for tungsten, the element with the highest melting point and tensile strength, is reshaping worldwide critical mineral trade flows, roiling markets, and sparking conflicts.

In this Article

- Tungsten is a strategic focus in global critical mineral trade due to its defense and industrial applications.

- Holding over 80% of global tungsten output, China dominates and is shaping trade policy and export controls.

- U.S. reliance on China is declining, with increased use of recycled tungsten and diversified import sources.

- Trade tensions are rising, with tariffs and restrictions on tungsten intensifying between the U.S. and China.

- Data from Descartes Datamyne helps track sourcing shifts, identify risks, and support critical mineral trade decisions.

The U.S.-Ukraine minerals deal signed April 30 doesn’t cover tungsten (mined in Russia, but not in Ukraine). But the conflict in Ukraine has added urgency to the quest to secure critical mineral trade, starting with tungsten, an essential element in munitions manufacturing. The three-year conflict has depleted weapons stockpiles and boosted defense budgets as Europe re-arms.

Tungsten has specific applications as well, from filaments in incandescent lightbulbs to tungsten carbides and alloys used to make cutting and wear-resistant tools for construction, metalworking, mining, and oil- and gas-drilling. With deposits to be found on every continent (except Antarctica), it is nonetheless in limited supply, with the majority of tungsten production concentrated in China (see Figure 1).

Figure 1 The World’s Tungsten Reserves

Source: International Tungsten Industry Association.

Although there are as many as 100 U.S. sites with tungsten deposits, the U.S. Geological Survey reports that tungsten has not been mined commercially in the U.S. since 2015. The U.S. has long identified tungsten as one of the critical minerals of strategic importance to the country’s security and economy. But the costs of digging and processing the ore have far exceeded the price tungsten could command in global markets.

However, as The Economist commented in February, rare elements often turn out to be less rare when there is a powerful incentive to find new sources.

China’s Advantage in Tungsten and Critical Mineral Trade

The world’s top producer of tungsten (as well as 29 other minerals on the U.S. critical list), China has been leveraging this competitive advantage in its trade dispute with the U.S., reshaping critical mineral trade relations globally.

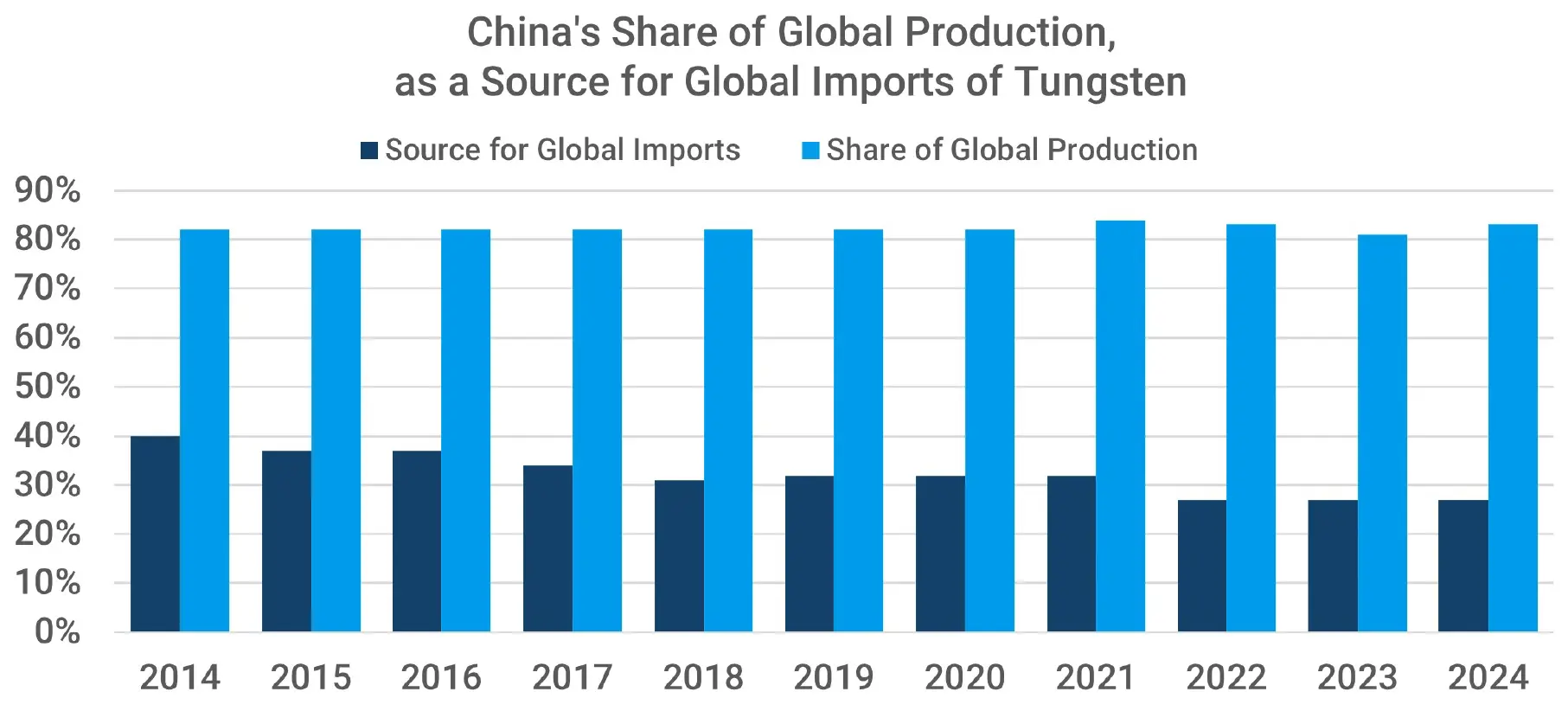

The United States Geological Survey (USGS) reports China’s share of global production of tungsten has held steady at 80%-83% over the past decade. Over the same period, China’s share of exports available for purchase in the global market has declined from 40% in 2014 to 27% in 2024 (see Figure 2), a trend that affects global critical mineral trade dynamics.

Figure 2 China’s Share of Global Tungsten Reserves and Sourcing of Tungsten Imports

Source: U.S. Geological Survey.

China has been augmenting its domestic stockpiles with more imports, as the World Trade Organization’s data on China’s critical mineral trade shows (see Figure 3).

Figure 3 Top Importers of Critical Minerals

Source: WTO analytical database.

Descartes Datamyne China data indicates that tungsten is part of the surge in imports (see Figure 4). Note that the Chinese Harmonized System (HS) tariff code HS261100 covers ores and concentrates; tungsten is generally traded in its concentrate form.

Figure 4 China’s Imports of Tungsten Ore & Concentrates

Source: Descartes Datamyne U.S. Census import data.

Data on China also documents the sources for these imports (see Figure 5).

Figure 5 Countries of Origin for China’s Imports of Tungsten Ores & Concentrates

Source: Descartes Datamyne U.S. Census import data.

According to the Financial Times, China has been building up its mineral resources both at home and abroad. Over the past year, at least half of China’s provincial governments, including those of mineral-rich regions such as Xinjiang, have increased subsidies or expanded access for mineral exploration. Over the past two decades, China has also been investing in mining enterprises across the developing world. These investments are not Belt and Road loans, but most often joint ventures in which Chinese entities share ownership.

Critical mineral trade – tungsten in particular – is very much in play in the U.S.-China trade dispute.

China introduced tungsten export licensing in August 2023. In September 2024, the Biden Administration extended tariffs to tungsten concentrates, oxides, tungstates, and carbides. When the Trump Administration ratcheted up its tariffs on Chinese goods another 10% on February 1, China countered three days later by restricting exports of five critical metals: tungsten, tellurium, bismuth, indium, and molybdenum.

U.S. Reliance China

While China has been buying tungsten, the U.S. appears to be cutting back on imports (see Figure 6).

Figure 6 Comparison of Chinese and U.S. Imports of Tungsten Ores & Concentrates

Source: Descartes Datamyne U.S. Census import data.

Note that, as with the China data above, the 6-digit HS code covers both ores and concentrates. Data at U.S. 8-digit tariff code level distinguishes between the two and establishes that ores accounted for 1% of these imports in 2018, 3% in 2024.

Not only does the U.S. appear to be buying less of the mineral, it is also importing from fewer countries (see Figure 7).

Figure 7 Top Countries of Origin for U.S. Imports of Tungsten Ores & Concentrates 2018 vs. 2024

Source: Descartes Datamyne U.S. Census import data.

In 2018, China was well down the list of U.S. suppliers, accounting for 0.02% of these imports. In 2024, imports from China jumped to US$1.6 million from 2018’s US$16,600. Russia, source for 6% of this trade in 2018, exported no tungsten, in any form, to the U.S. in 2024.

U.S. imports of tungsten ores & concentrates, along with ammonium tungstates (ammonium paratungstate – or APT) [HS2842800], both of which might be considered feedstocks, peaked in 2018. That was the year that the U.S. finalized its list of the 35 critical minerals that were to be the focus of a multi-agency government strategy to break America’s dependence on foreign resources—an initiative directly tied to critical mineral trade policy.

To get a more complete picture of U.S. tungsten resources, the USGS watches not only feedstocks but also forms of tungsten up the value chain. These include tungsten oxides [HS28259030], tungsten waste & scrap [HS810197], tungsten powders [HS81011000], tungsten carbides [HS28499030], and ferrotungsten and ferrosilicon tungsten [HS720280000]. When the trade data for all these forms of tungsten is totaled, it emerges that China’s imports have surpassed those of the U.S. only in the past year (see Figure 8).

Figure 8 Comparison of Chinese & U.S. Import of Tungsten Materials 2014-2024

Source: Descartes Datamyne U.S. Census import data.

Data from Descartes Datamyne shows that most tungsten imports from China are feedstocks – ores & concentrates, APT, and oxides – from just shy of 90% in 2018 to 98% in 2024. China has not imported tungsten waste & scrap since 2017.

The Challenge of Decoupling

Although China makes a negligible contribution to U.S. import of tungsten ores & concentrates, when imports of all the USGS-identified forms of tungsten are counted, the ongoing (but waning) reliance of the U.S. on China remains an ongoing critical mineral trade concern (see Figure 9).

Figure 9 Top Countries of Origin for U.S. Imports of Tungsten Materials 2018 vs. 2024

*Tungsten or, concentrates, APT, oxides, powders, cabides, ferrotungsten, waste & scrap.

Source: Descartes Datamyne U.S. Census import data.

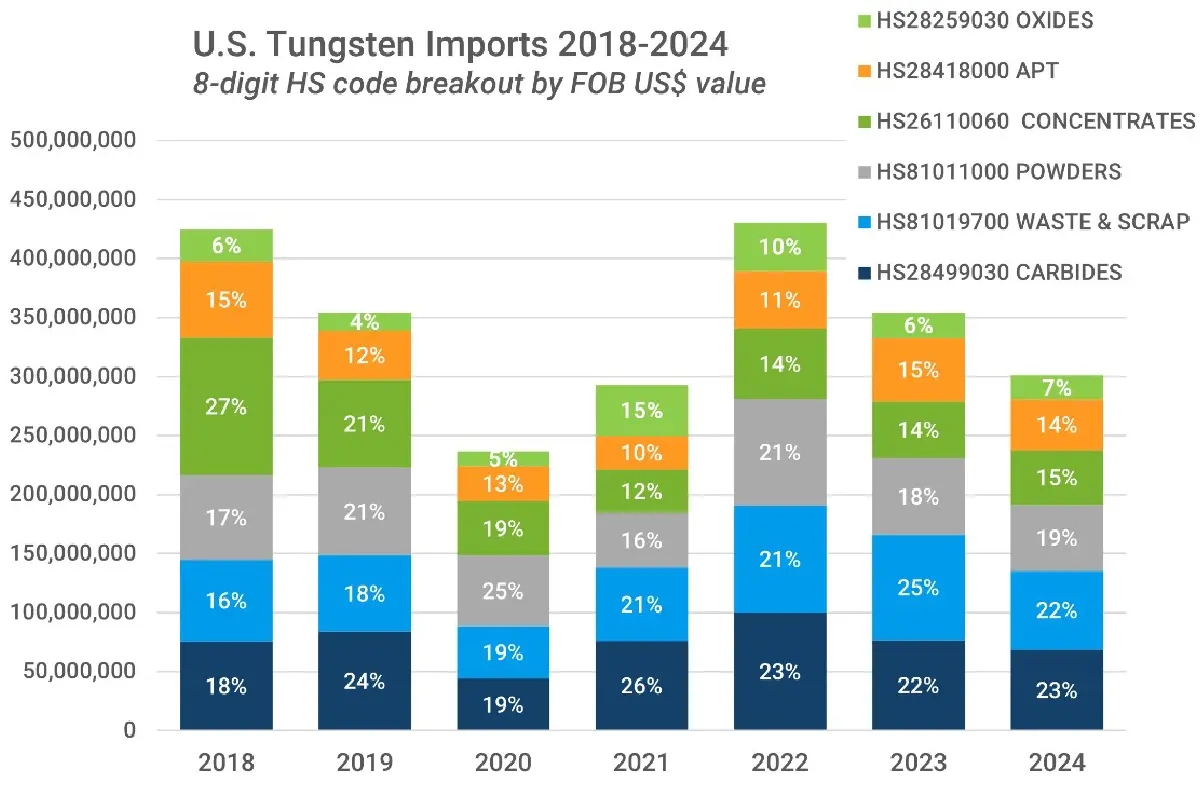

Figure 10 offers a breakout of the raw and processed materials that make up this trade. (Note that ferrotungsten and ferrosilicon tungsten account for 1% or less of imports of tungsten materials; ores for 1%-3%. These tariff codes are not included in the breakout chart.)

Figure 10 Breakout of U.S. Imports of Tungsten Materials by 8-digit HS code 2018-2024

Source: Descartes Datamyne U.S. Census import data.

According to the USGS, there are seven U.S. companies able to convert tungsten concentrates, APT, tungsten oxides – or scrap – into the tungsten powders or carbides used to make cutting and wear-resistant carbide parts, alloys, and specialty steels. The trade disruptions of 2020-22 challenge trend spotting. But, with concentrates dropping from a 27% share of U.S. imports in 2018 to 15% in 2024, while waste & scrap climbed from 16% to 22%, it looks like there has been a shift by processors away from the raw material and towards recycled tungsten, reflecting a shift in efforts to localize critical mineral trade inputs.

Certainly, the growing reliance on recycled tungsten has been accompanied by some decoupling from China as a feedstock source (see Figure 11).

Figure 11 Top Countries of Origin for U.S. Imports of Tungsten Waste & Scrap 2018 vs. 2024

Source: Descartes Datamyne U.S. Census import data.

Critical mineral trade data also indicates an upward tick in imports of downstream materials: from 17% in 2018 to 19% in 2024 for tungsten powders; from 18% to 23% for tungsten carbides for the same two years (see Figure 12). The progress towards alternative sources for tungsten powder is particularly striking.

Figure 12 Top Countries of Origin for U.S. Imports of Tungsten Powder 2018 vs. 2024

Source: Descartes Datamyne U.S. Census import data.

More to Come

The U.S. strategy to unlock any stranglehold on tungsten supplies – or other critical mineral trade targets – is four-fold: find substitutes, secure access to diverse foreign sources, mine domestic deposits, and recycle more existing materials [see, for instance, the U.S. Dept. of Energy Critical Minerals and Materials Program].

As the Descartes Datamyne trade data indicates, since 2018 the U.S. has made progress in diversifying its foreign sources for tungsten. This will continue to be its strategic priority in critical mineral trade– although tactical approaches will change, often abruptly. The Biden administration set a 2027 deadline for the U.S. military to halt all procurement of tungsten mined or manufactured in China and Russia, the world’s third-largest producer. Steep duties were set for tungsten imports as part of the Trump administration’s April 2 “Liberation Day” tariffs, currently suspended (and, as of this writing, being re-negotiated).

More stringent controls and tighter deadlines may be in the offing. On April 15, the U.S. opened an investigation into processed critical minerals and derivatives. The executive order (EO) directed the Commerce Department to submit an interim report in 90 days.

The U.S. is also looking further afield for resources. An April 24 EO directs multiple government agencies to take steps to facilitate exploration and development of seabed mineral resources. The U.S. is reported to be in talks on mineral rights with the Democratic Republic (D.R.)of Congo. Critical mineral trade resources are a geopolitical flashpoint in Africa where armed conflict has broken out between D.R. Congo and Rwanda, the world’s second biggest producer of tungsten.

There are moves to reopen tungsten mines in the U.S. and its trading partners. Drilling has restarted at South Korea’s Sangdong mine, closed in 1994 because it couldn’t compete with less costly tungsten from China, as The Straits Times reports. In North America, a Canadian-based company is developing mining resources in Idaho.

How Can Descartes Help?

Companies navigating global markets for sources of supply in times like these are looking at the same four options as U.S. trade policymakers: find substitutes, secure access to diverse cross-border supply chains, look to domestic resources, and recycle more existing materials.

Descartes Datamyne trade intelligence is a vital resource for analyzing global critical mineral trade.

Start with Descartes CustomsInfo™. As the Wall Street Journal correctly notes, customs brokers are in high demand for their “arcane knowledge” as the U.S. attempts to rebalance its trading relationship by wielding tariffs. Descartes CustomsInfo provides easy access to current information on tariff-code classification, import duties, and restrictions on cross-border commerce. The solution also automates the comparison of shopping based on the landed costs of shipments; and helps assure that transactions are in compliance with current regulations.

Here are five good reasons to stay on top of today’s rising tide of tariffs and trade restrictions with Descartes CustomsInfo.

Look to Descartes Datamyne trade data to discover rising production hubs, identify disrupted trading relationships, and track global market dynamics – including shifts in critical mineral trade. Descartes Datamyne U.S. bill of lading data, released within two days of shipment arrival, documents the buyers and sellers that make markets – and the sources and customers they rely on.

Request a demo and we’ll show you how.