When in the midst of a challenging journey, most of us check the progress we are making, however slow, by looking for the light at the end of the tunnel. As part of Descartes’ ongoing update on the global shipping crisis, we will examine key logistics and economic data to try to see if the situation is improving. Here are the latest data points:

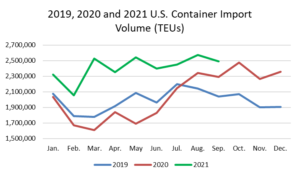

U.S. Import Container Volume Remains High.

Compared with August, September is slightly lower, but compared year on year the numbers are significantly higher (See Figure #1). Overall, September this year was 9% above the same month last year and 22% higher than the pre-pandemic period of 2019, according to trade data from Descartes Datamyne. In general, TEU volume will likely continue hovering around the 2.4 million and 2.6 million TEU ranges monthly until the Fall of 2022.

Figure #1. U.S. Container Import Volume Year-over-Year Comparison

Why 24×7 Will Not Reduce the Congestion

Overall, port entry delays are down slightly. So far this month, the estimated delay for a vessel entering the Port of Los Angeles is 14.5 days. This is a decline from the peak of 15.3 days that we saw in August. For context, the estimated delay in October of last year was 4.5 days/

The proposed increase in operating hours for the Port (a proposal that is likely to spread to other ports), while certainly helpful, is only estimated to improve throughput by roughly 3,500 containers per week; however, the Port of LA already is handling more than 80,000 containers per week based on averages over the last several months.

What are Carriers and Logistics Service Providers Saying?

Logistics managers and transportation industry operators continue to emphasize that their businesses remain at max capacity and that the current situation is unlikely to improve in the near future – they are not expecting a decline in shipping demand through the rest of 2021 and well into 2022. The warning from these professionals is that carriers simply are not able to keep up with demand and this has resulted in ships being packed beyond capacity and produced increased container “rolling” rates.

Retailers are Still Behind on Inventory Levels

Inventory to sales ratios (see Figure #2) have improved slightly but remain almost 32% lower than last year. In addition, many retailers have stated that they will carry more inventory going forward. Closing the retail inventory to sales ratio gap and exceeding it will continue to put pressure on global logistics providers beyond the holiday peak season and well into 2022.

Figure #2: FRED Retail Inventory to Sales Ratio

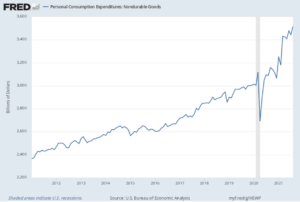

Consumers are Continuing to Embrace the “Stuff Economy”.

While still dealing with the current crisis, there are several factors that could result in even more long-term shipping volume increases. Many consumers continue to do well economically, but no longer spend their disposable income on “experiences” such as international travel or even local experiences like restaurants and theatres. These consumers are, instead, buying durable and non-durable goods at very strong rates (See Figures #3 and #4). The implication for global shipping is that many of these goods are produced outside of the U.S. and will need to be imported – increasing overall demand and prolonging the capacity crunch.

Figure #3: Personal Consumption Expenditures: Durable Goods Figure #4: Personal Consumption Expenditures: Nondurable Goods

Are We There Yet?

From a high-level perspective, it’s safe to say at this point that we are not close to “there yet”. The data continues to suggest that importers view the global logistics capacity shortage as more than a short-term problem.

Descartes will continue to highlight Descartes Datamyne and U.S. trade data monthly to give importers and logistics services providers a better view into the continuing global shipping crisis. In the meantime, importers should: a) evaluate product mix to only focus on their high velocity SKUs for the limited transportation capacity available to minimize cash cycles with limited available inventory; b) shift their movement of goods to less congested lanes to improve supply chain velocity and reliability and c) evaluate supplier and factory location density to mitigate reliance on over-taxed trade lanes.

Get the Essential Guide to Supply Chain Resiliency

As carriers and ports work through the global shipping crisis and the subsequent backlog, now is the time for you to invest in your supply chain resiliency.

Our essential guide has been developed to help you mitigate risks and protect your business from costly disruptions.

Notes

-

Descartes Datamyne

-

Fact Sheet: Biden Administration

-

Port of Los Angeles